Climate Risks & Opportunities

Climate Action

On January 15, 2025, the World Economic Forum (WEF) released the "Global Risks Report 2025," in which “extreme weather events” remained the top long-term risk over the next ten years, reflecting respondents' deep concern over the ongoing global climate crises. Since the first "Global Risks Report" was published in 2006, environmental impacts have shown a worsening trend in both intensity and frequency. This year' s report indicates that nearly all environment-related risks ranked among the top ten long-term risks over the next decade. Respondents expect “extreme weather events” to become even more severe, marking the second consecutive year it has topped the list of long-term risks—painting a pessimistic outlook for environmental risk. Extreme weather events are becoming increasingly frequent and destructive; over the past 50 years, the cost per climate disaster has risen by nearly 77%. These climate change-driven extreme weather events have had widespread global impacts, disproportionately affecting the most impoverished communities.

As the threat of global climate change becomes increasingly evident, governments worldwide are actively formulating regulations, enhancing climate change mitigation efforts, and setting net-zero emission targets. Financial institutions, serving as intermediaries of capital, play a crucial role in steering sustainable development. Beyond reducing their own operational carbon footprints, they have a responsibility to promote the rational allocation of capital through financial tools and mechanisms, guiding businesses towards achieving low-carbon transitions.

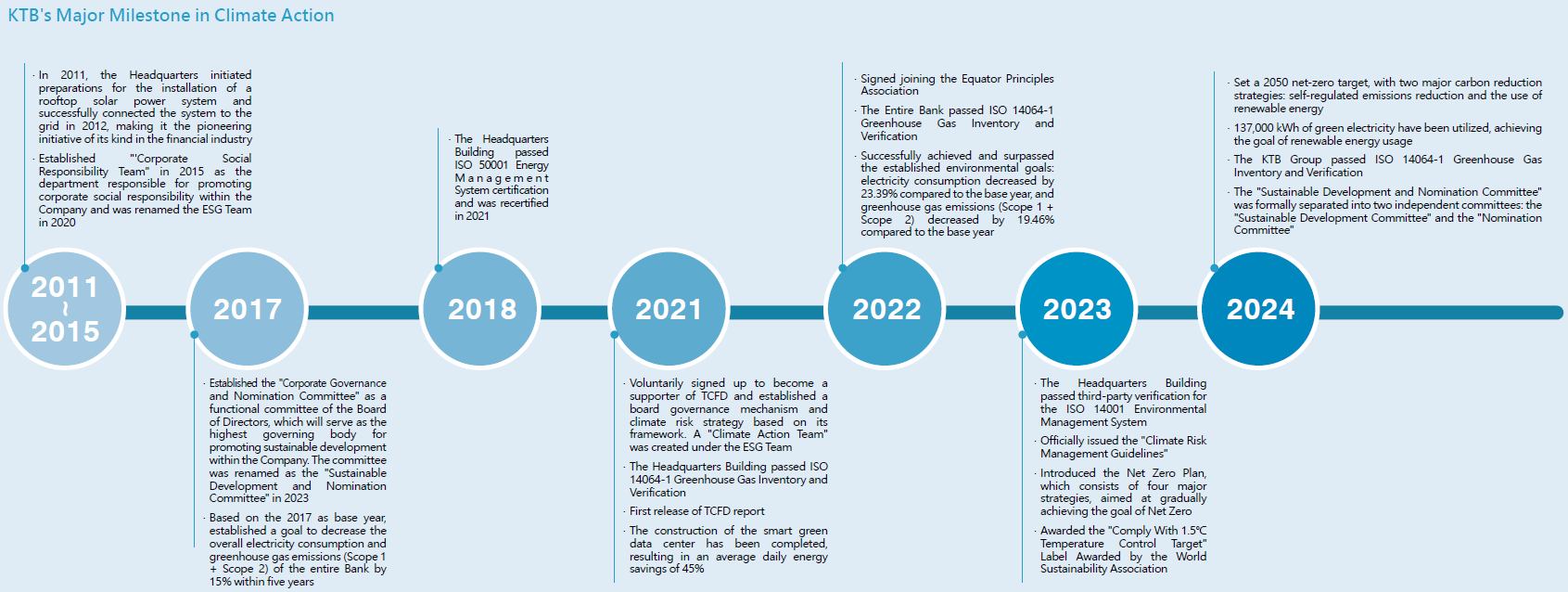

KTB, in response to global climate action, signed the Task Force on Climate-related Financial Disclosures (TCFD) in July 2021. Following the TCFD framework, KTB made its first related disclosures in its 2021 Sustainability report and has continued to enhance its understanding and management of the financial impacts of climate risks each year. Since 2022, in accordance with the “Scenario Analysis of Climate Changes by Domestic Banks in 2022” issued by Taiwan' s competent authorities, KTB has implemented and enhanced the management of climate-related risks and the transparency of related information. In addition, in 2023, the Board of Directors approved the "King' s Town Bank Climate Risk Management Guidelines" to enhance the Company's assessment of potential climate change risks and opportunities. This development includes measures for mitigating and adapting to climate risks, thereby improving the Company's capacity for climate change risk management.

Governance

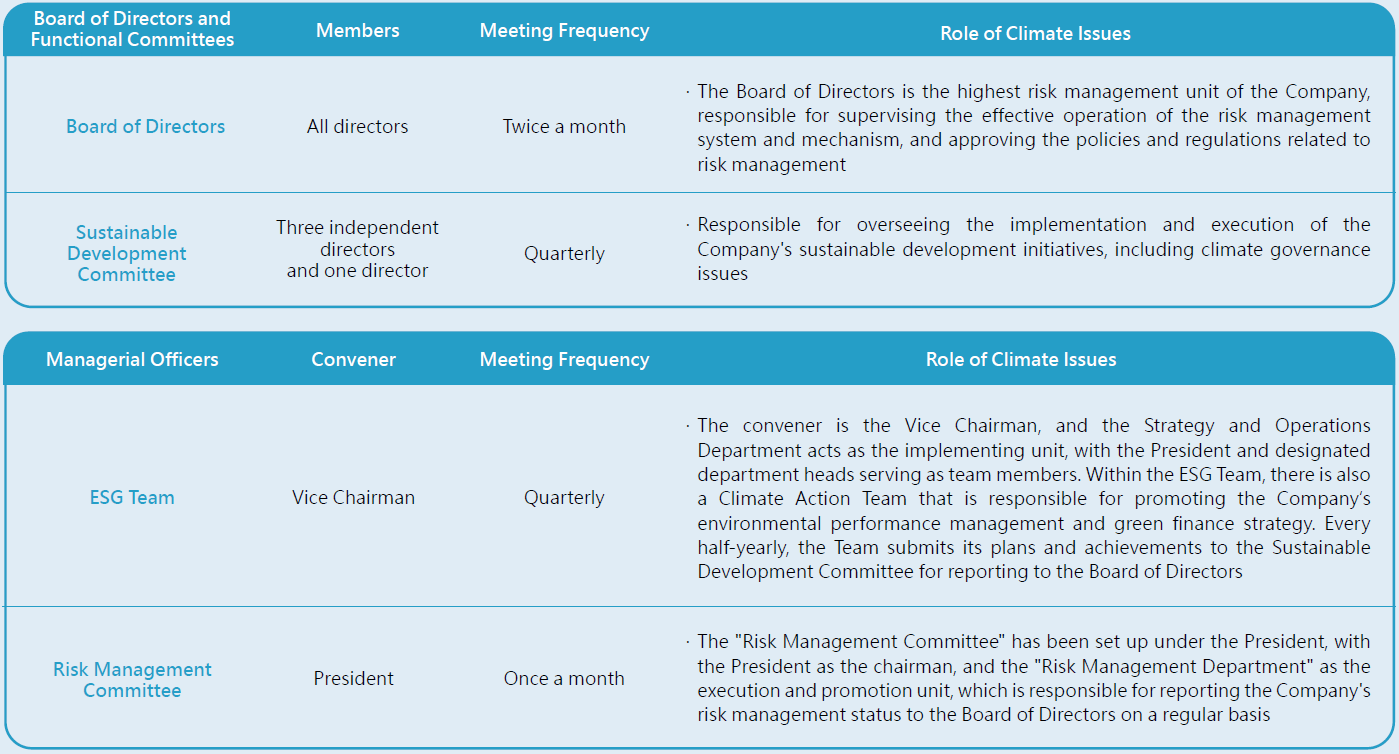

KTB has established a climate-related risk management structure and system by integrating it into the enterprise risk management framework. The Board of Directors serves as the highest governance body for climate related issues and holds ultimate oversight and responsibility. Under the Board of Directors, the Sustainable Development Committee is established, and beneath it, a cross-departmental ESG Task Force is responsible for implementing sustainability initiatives. In response to climate change issues, a Climate Action Team has also been formed to identify and assess climate-related risks and opportunities, assist in developing relevant quantitative methods and indicators internally, and formulate climate-related management measures. The ESG Task Force reports the implementation status of sustainability initiatives, including climate-related matters to the Sustainable Development Committee half-yearly, which is then submitted to the Board of Directors.

In addition, under the supervision of the President, the “Risk Management Committee” has been set up. The committee comprises heads of various departments, including the Treasury Department, Digital Service and Channel Management Department, Risk Management Department, Credit Assessment Department, Administration Management Department, International Banking Department, Compliance Department, and Strategy and Operations Department. The Risk Management Department serves as the executing unit, responsible for overseeing the bank' s climate risk management mechanisms, formulating climate risk management guidelines, and integrating climate risk management into the overall risk management process. Each year, the Risk Management Department reports the Company' s climate-related financial information and the quantified financial impacts to the Board of Directors.

Training Programs

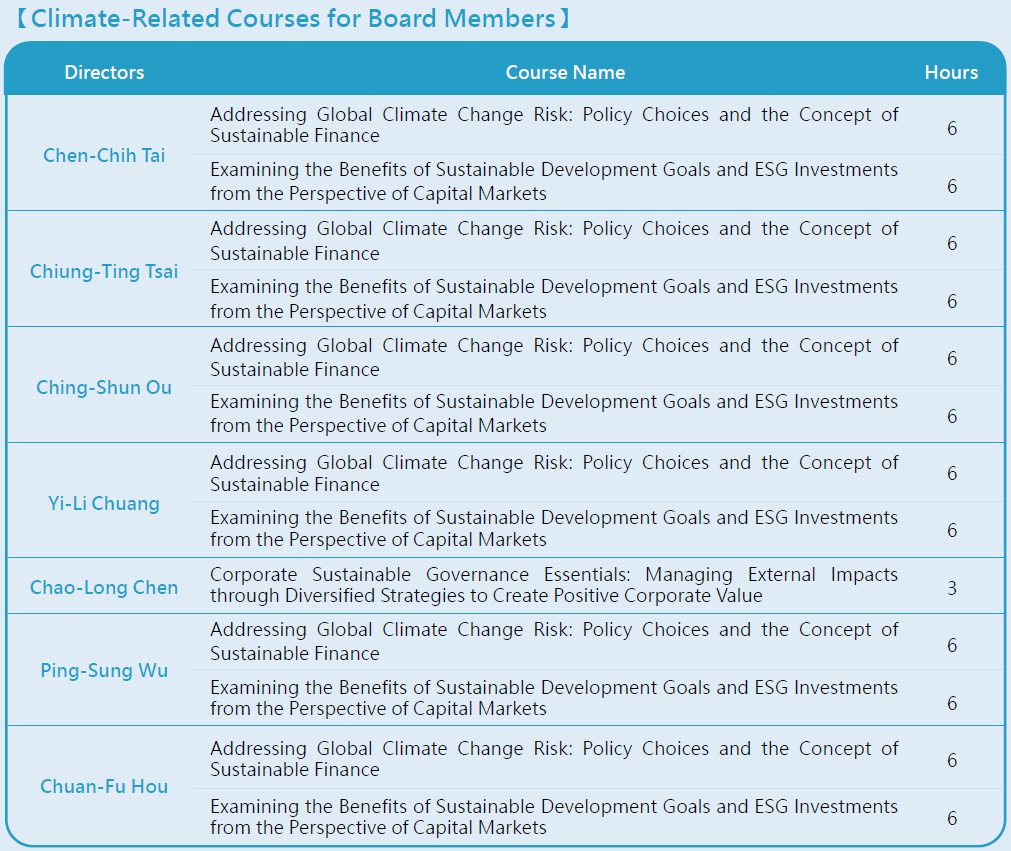

To strengthen the awareness and response capabilities of the Board of Directors and senior management regarding climate issues, KTB regularly conducts training sessions for board members and senior executives on climate change and sustainable finance. The training covers key topics such as domestic and international policy trends, low-carbon transition strategies, and the TCFD framework. These efforts aim to move from raising awareness to integrating climate issues into practical operations and embedding climate governance into the Bank's core decision-making processes. In 2024, board members attended three climate-related training sessions, totaling 75 training hours.

In addition to the aforementioned training for the Board of Directors and senior executives, KTB also promotes sustainable finance literacy among all employees. For general staff, a three hours of sustainable finance training is scheduled per person annually. The training includes topics such as net-zero trends and green financial products, aimed at enhancing frontline employees' understanding of sustainable finance products and related risk issues, as well as improving their ability to engage with stakeholders on these matters. In 2024, a total of 959 employees completed general sustainable finance training, accumulating 2,877 training hours.

Furthermore, KTB encourages designated departments to proactively participate in advanced external training programs to stay abreast of the latest policy trends and practical approaches. This helps enhance professional competencies, foster experience sharing, and promote the in-depth and cross-functional implementation of climate and sustainability initiatives within the Company. Topics covered include sustainable finance, net-zero carbon reduction, climate change and risk, IFRS S1 & S2, and carbon pricing. In 2024, employees participated in 15 climate and sustainability-related professional training sessions, totaling 28 participants and 187.5 training hours.

Incentive Mechanism

The Company clearly stipulates the standards and procedures for allocating directors’ remuneration in its Articles of Incorporation. The ratio and amount of remuneration granted to directors take into consideration factors such as industry benchmarks, the Company's financial and operational performance, and the results of Board of Directors performance evaluations. The Board of Directors performance evaluation includes the Board’s oversight and promotion of sustainable development. The evaluation results are submitted annually to the Remuneration Committee and the Board of Directors for approval and are subsequently reported at the shareholders’ meeting.

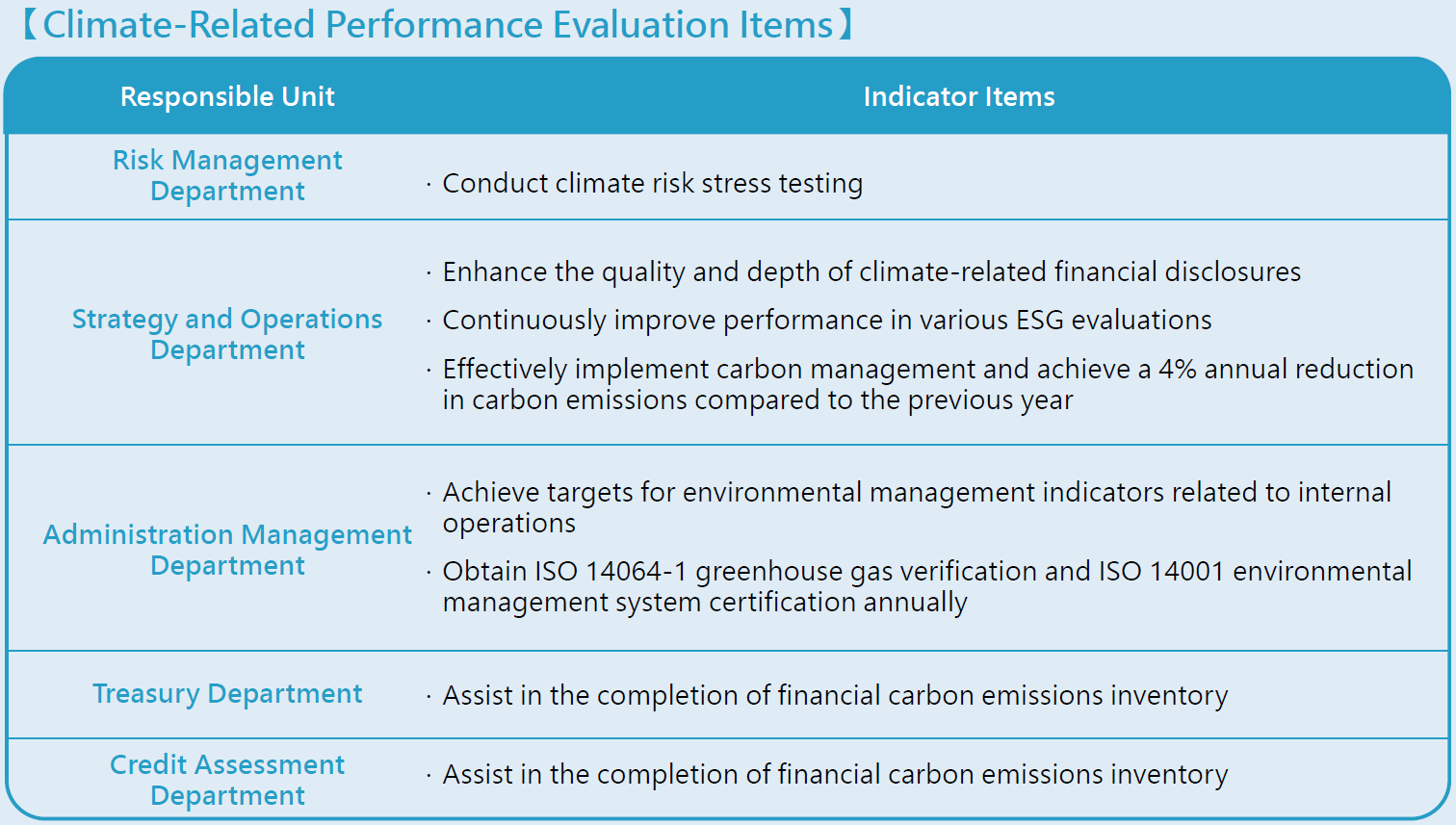

According to KTB’s “Regulations on the Annual Employee Performance Evaluation” and“Year-End Bonus Distribution Guidelines,” the annual compensation of senior management is closely tied to the "Performance Items of the Headquarters' Management Units." Among the performance indicators, the weight of the “ESG Implementation” key performance indicator must not be less than 5%, to ensure the effective advancement and execution of ESG initiatives.

Strategy and Risk Management

KTB's climate-related management strategy mainly focuses on three aspects, which is taken as the direction for optimization year-by-year:

.Manage climate-related risks, including physical and transition risks

.Manage the impact of the Company's operations on the climate

.Support customers in their transition to a low-carbon economy with financing or investment products

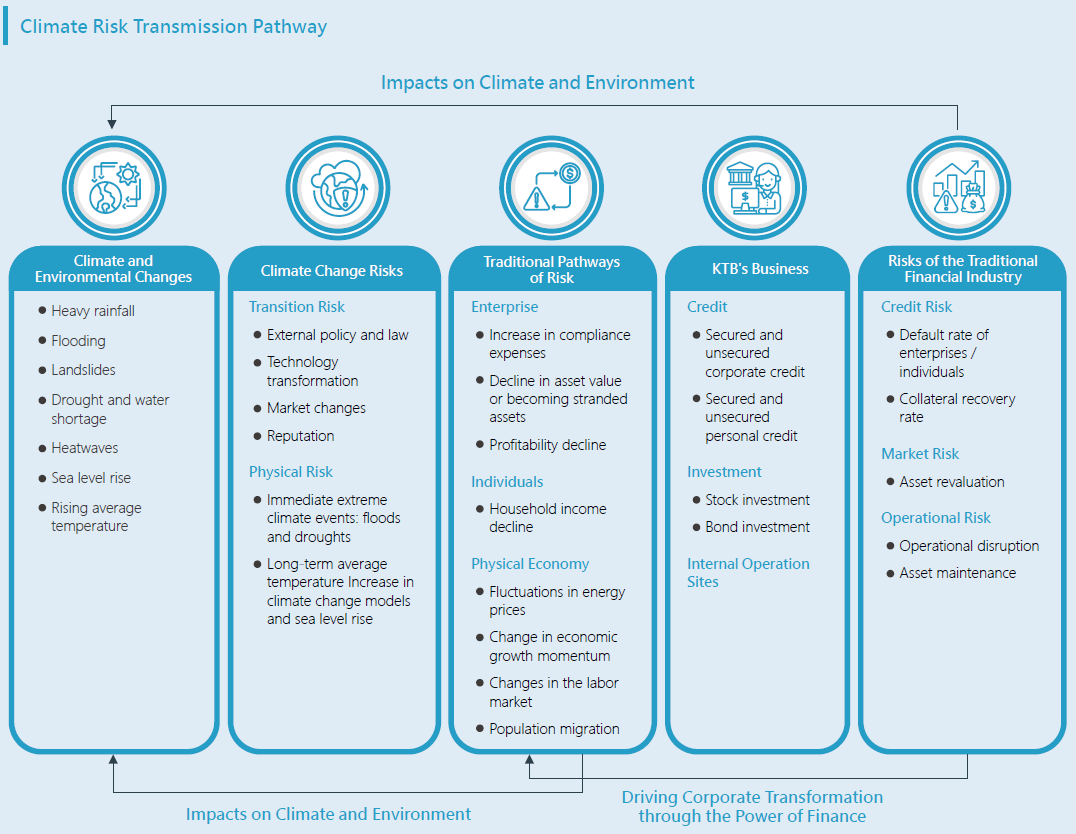

Regarding climate risk management, we believe that climate-related risks are not standalone risk categories but rather impact financial institutions directly or indirectly through transmission to individual and macroeconomic levels. This exacerbates traditional financial risks such as credit risk, market risk, operational risk, and others.

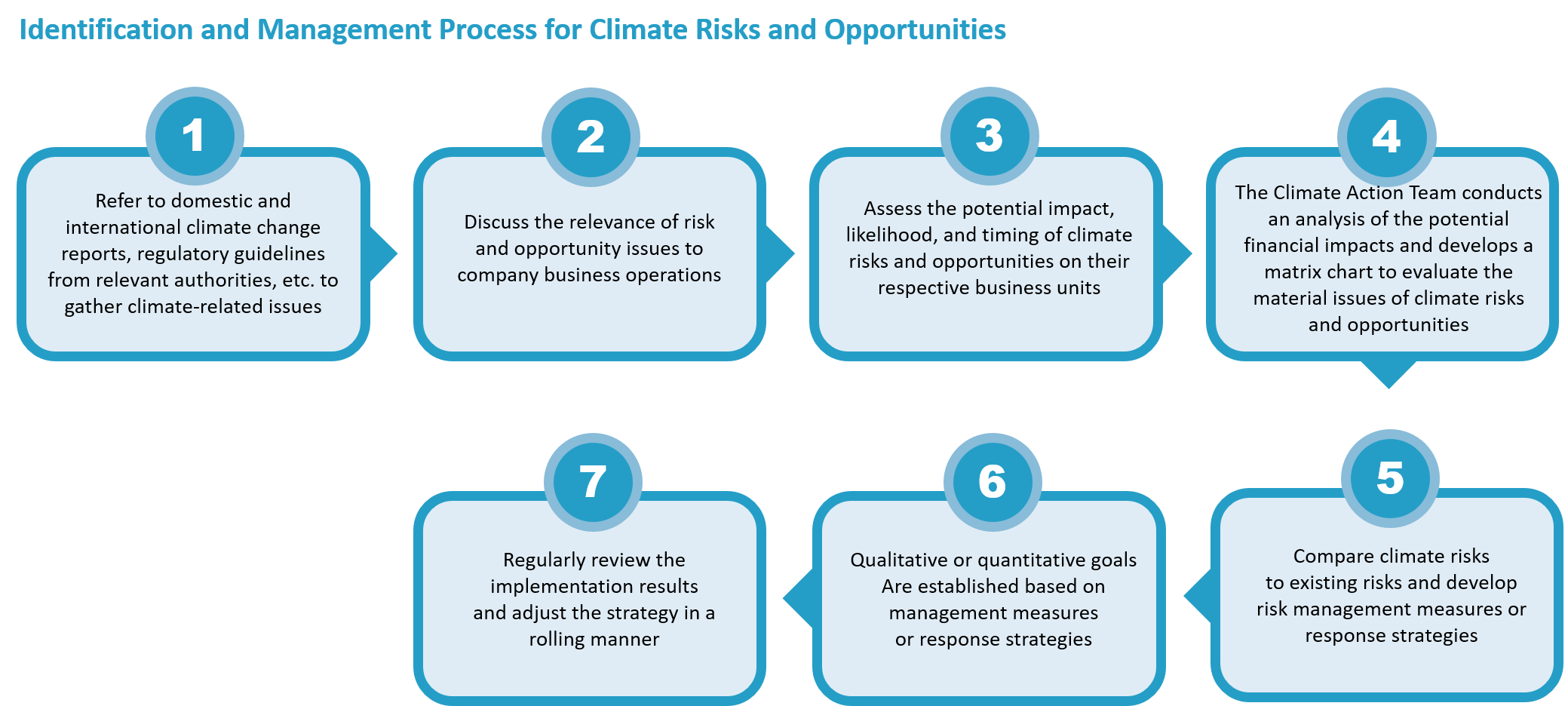

In order to comprehend the impacts and effects of climate change on the Company, the Board of Directors serves as the highest decision-making body for the Company's climate risk management framework. It determines comprehensive climate risk management guidelines and major decisions based on overall operational strategies and business environment assessments. Furthermore, within the ESG Team, a Climate

Action Team has been formed to identify and evaluate the risks and opportunities associated with climate change. The Team also aids in the development of quantitative methods and indicators, as well as the implementation of effective management measures. Regular reports on climate-related matters are submitted to the Risk Management Committee, which is responsible for overseeing the comprehensive framework and execution of the climate risk management mechanism.

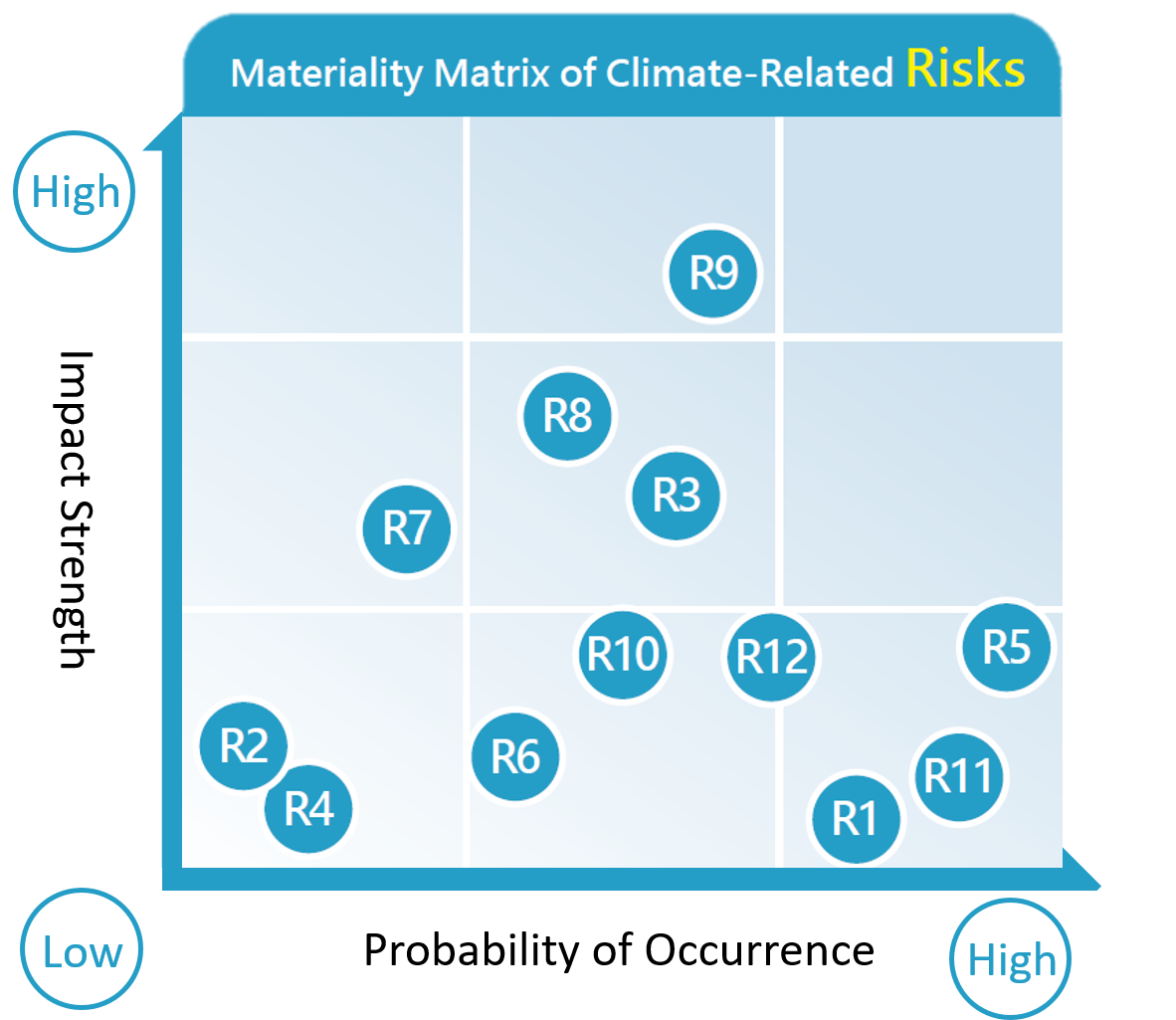

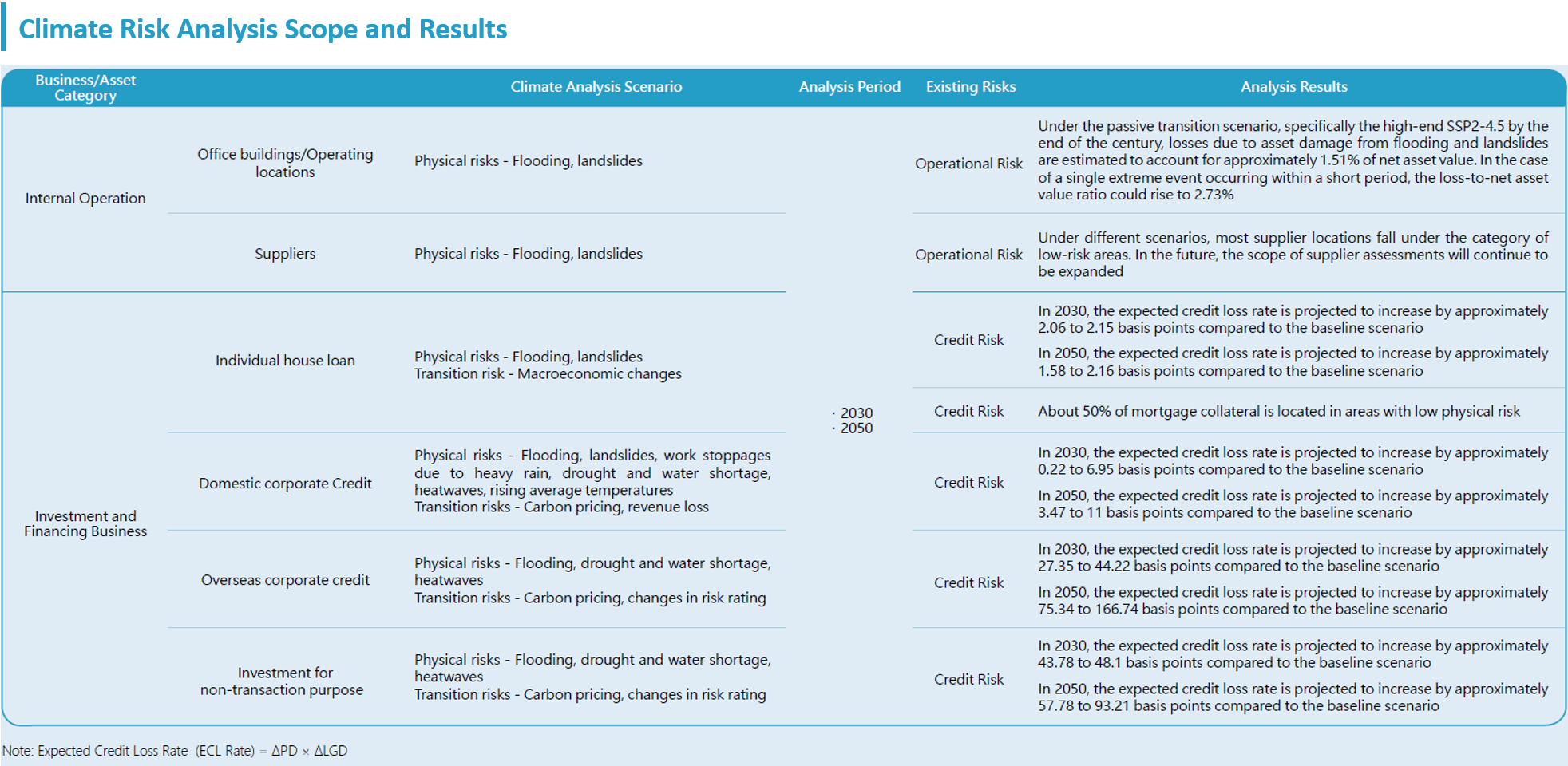

2024 KTB Climate-Related Risks

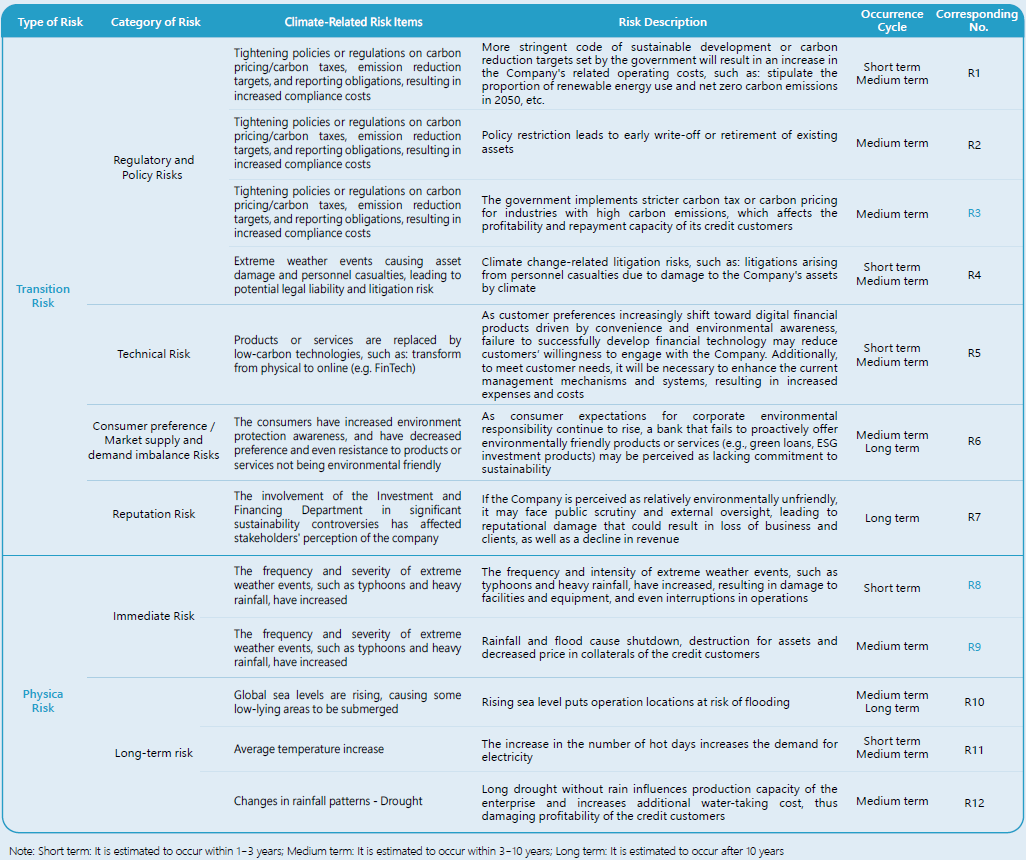

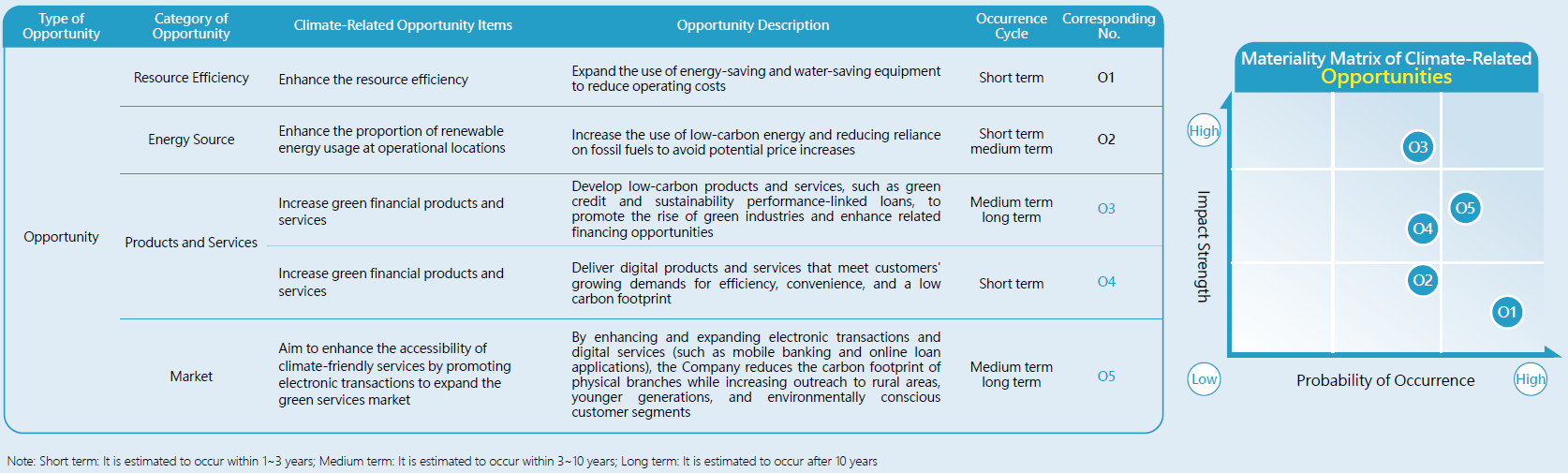

In alignment with the recommendations of the TCFD framework, the Company has identified a total of 12 climate-related risks and 5 climate related opportunities relevant to its business operations. Each business unit assessed these issues based on three key factors: the "timing of occurrence," the "likelihood of occurrence," and the "potential degree of impact on business." Based on this assessment, the Company developed a materiality matrix of climate related risks and opportunities. Members of the Climate Action Team then further evaluated the potential financial impacts and the correlation of these risks and opportunities with existing risk categories (e.g., credit risk, market risk, operational risk). Corresponding mitigation or adaptation strategies were subsequently formulated.

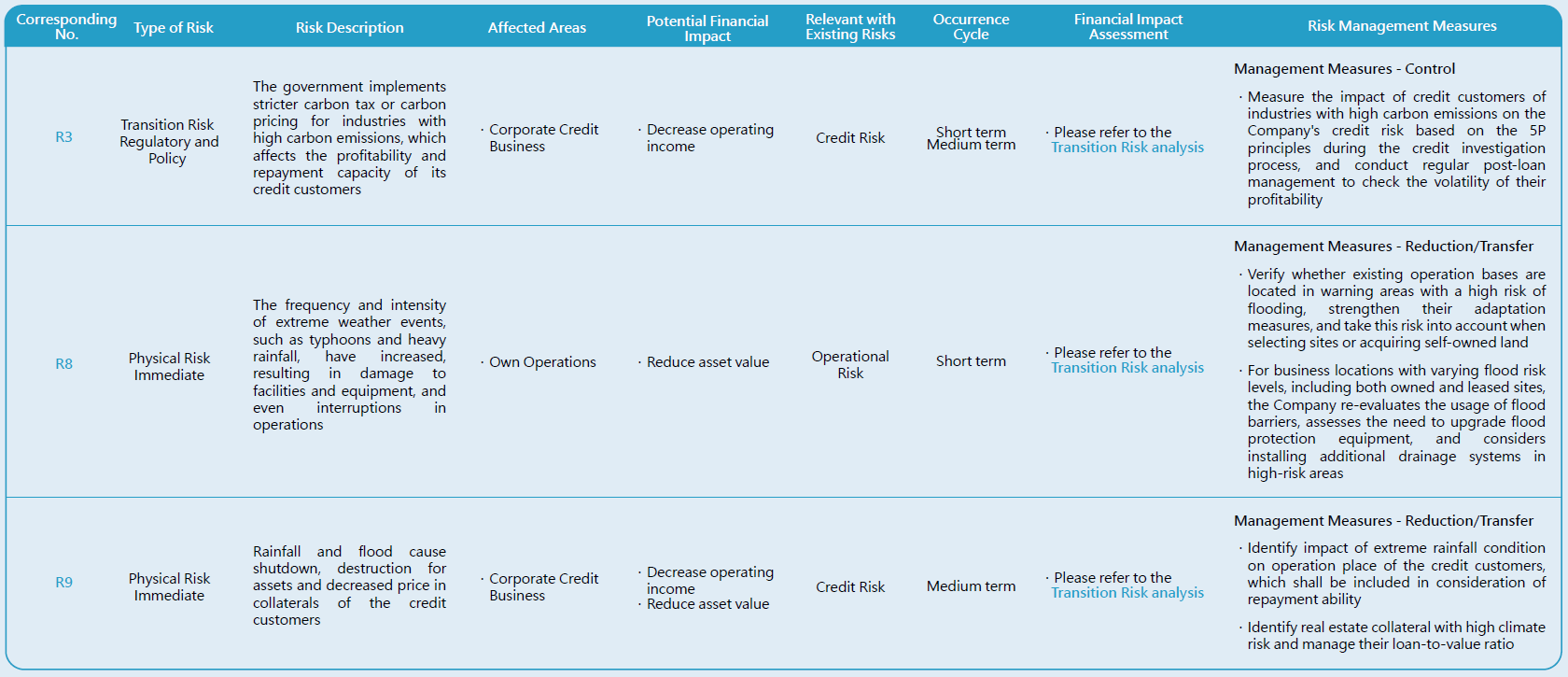

Based on the assessment of probability and impact, KTB has identified R3, R8, and R9 as relatively significant. For significant climate-related risks, the Company has implemented the following risk management measures:

Based on the assessment of probability and impact, KTB has identified O3, O4, and O5 as relatively significant. For significant climate-related opportunities, the Company has formulated following action measures

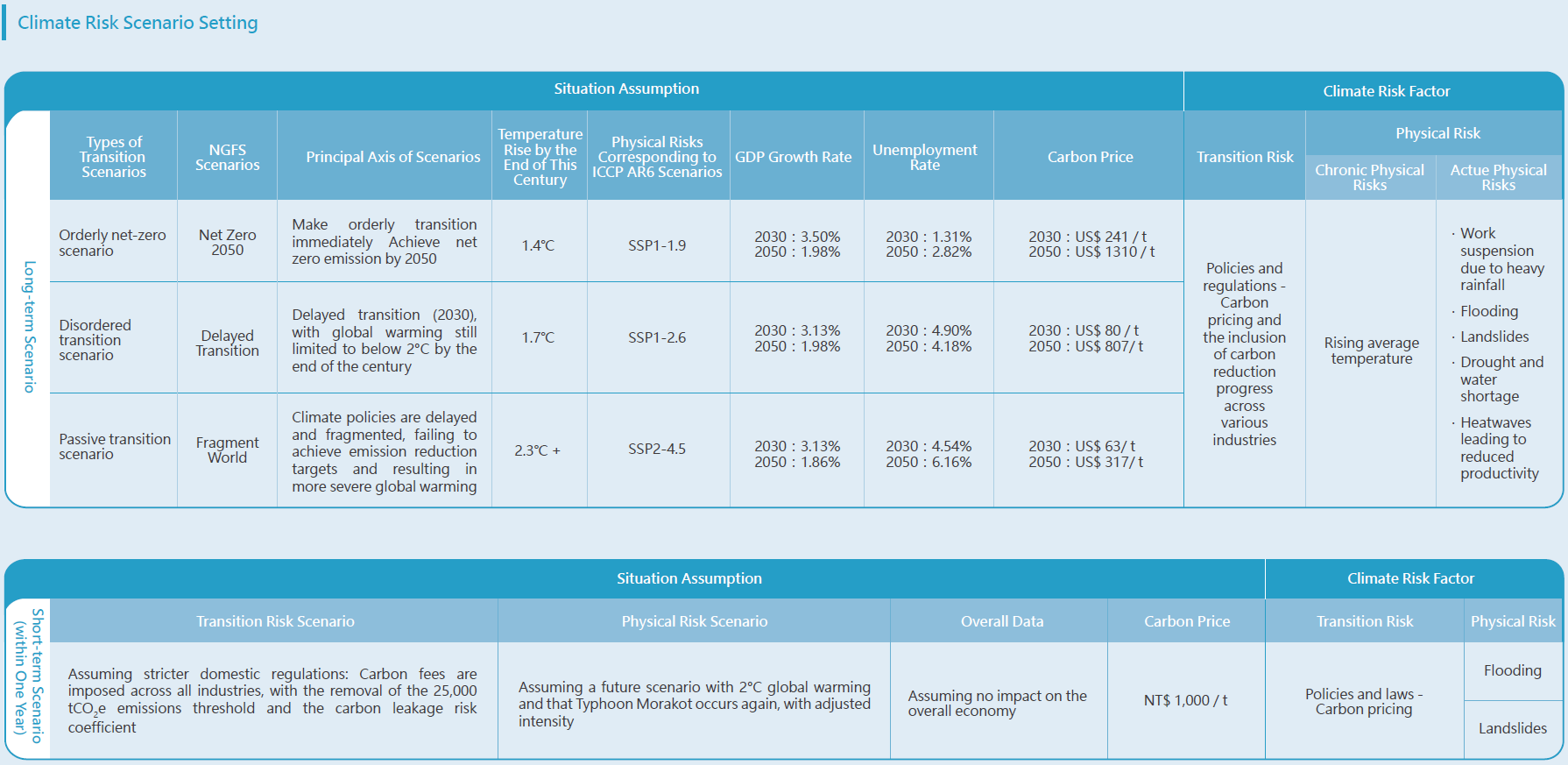

Assessing Strategy Resilience through Scenario Analysis

In accordance with the guidelines issued by Taiwan’s competent authorities on “Scenario Analysis of Climate Changes by Domestic Banks,” KTB adopted the Phase 4 scenario framework released in 2023 by the Network for Greening the Financial System (NGFS). The Bank selected the scenarios of Net Zero 2050, Delayed Transition, and Fragmented World as the primary basis for transition risk factors.

For physical risk factors, the Bank referenced the Intergovernmental Panel on Climate Change (IPCC) Sixth Assessment Report (AR6), utilizing the Shared Socioeconomic Pathways (SSPs) in conjunction with Representative Concentration Pathways (RCPs). These factors were then integrated and aligned accordingly to continuously strengthen climate risk management and enhance transparency in climate-related disclosures.

Comprehensive Result of Scenario Analysis

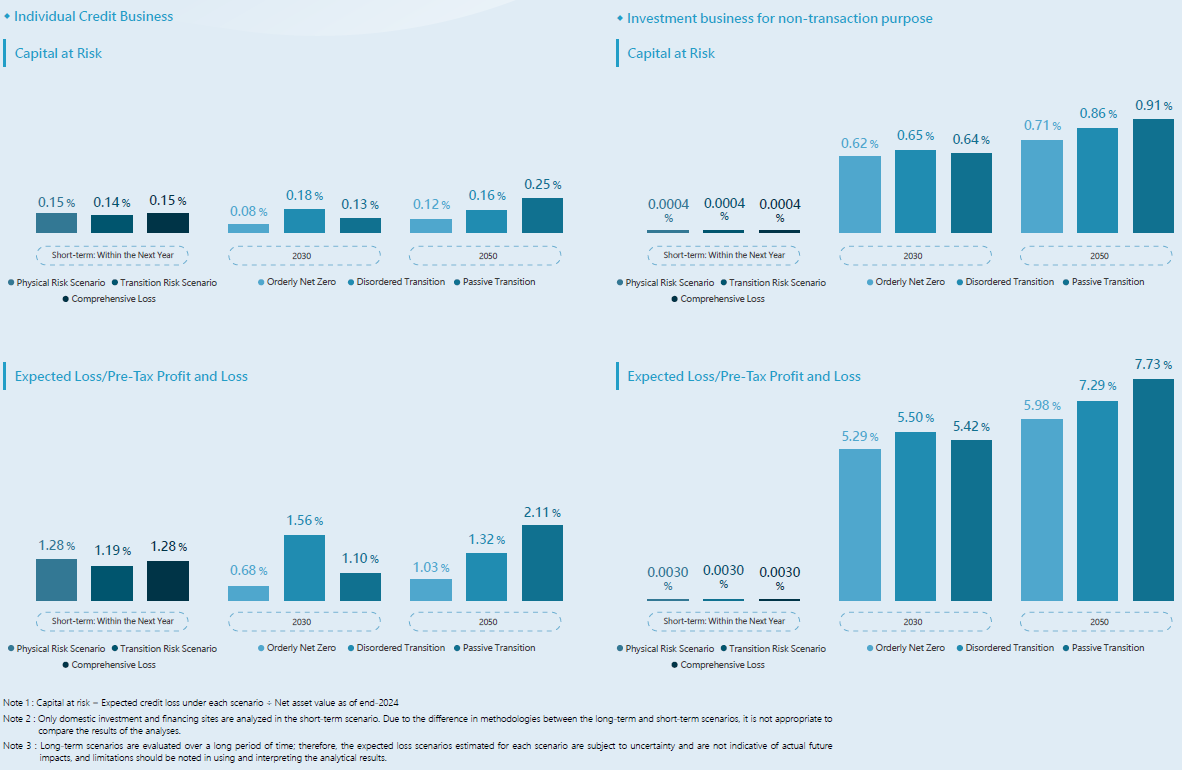

Under the aforementioned climate scenario framework, KTB assessed the potential impairment of assets at its own operating locations, as well as changes in credit risk parameters—Probability of Default (PD) and Loss Given Default (LGD)—for domestic and foreign credit, domestic and international bonds, and equity investments under stress conditions. The evaluation results are presented using Capital at Risk (i.e., expected credit loss amount ÷ baseline year net asset value).

Overall Investment and Financing Business

In the short-term scenarios, physical risks slightly outweigh transition risk scenarios and the overall loss outcomes, indicating that single-event physical disasters exert immediate pressure on credit and investment positions. However, the overall risk remains at a relatively manageable level. In long-term scenarios, the expected losses in 2050 are higher than those in 2030 across all scenarios, indicating that the overall climate risk intensifies over time. When comparing differences across scenarios, it is evident that under the disordered transition scenario, higher expected credit losses emerge in 2030, primarily due to rising carbon prices and a deteriorating macroeconomic environment. By 2050, the passive transition scenario exhibits the highest expected credit losses, mainly because transition risks begin to materialize while also facing significant impacts from physical risks.

Physical risk analysis - Flooding and landslides caused by heavy rainfall

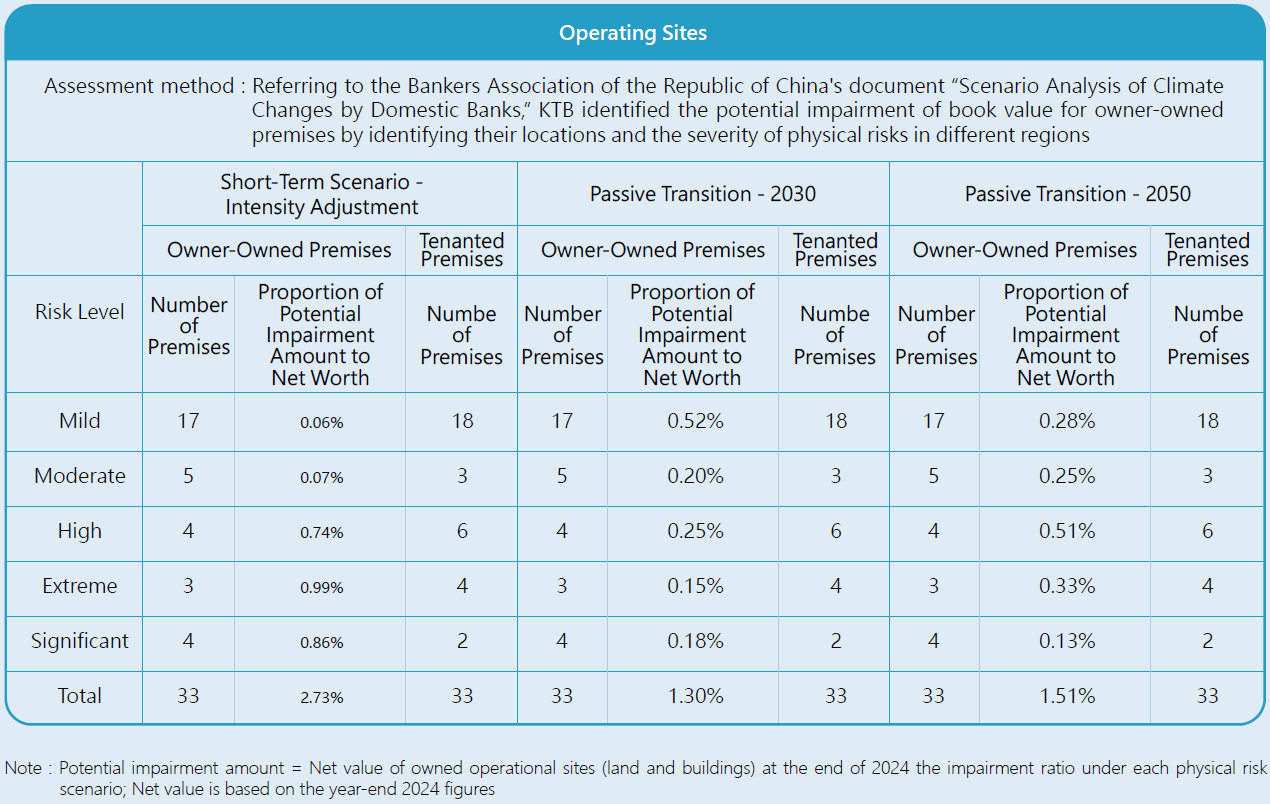

◆ Impairment of the Value of Owned Operational Sites

KTB's another major sources of revenue comes from over-the-counter banking services. If operational sites are flooded due to extreme weather conditions, it could result in business interruptions, asset and equipment write-offs, and potential impairment of owned asset values. This in turn increases operational risks for the bank. Therefore, KTB considers the depreciation losses from flooded operational sites as one of the significant climate risk factors.

KTB conducted an analysis of all owned operating sites using its climate risk analysis database to assess the distribution of risk levels, potential impairment amounts, and risk-bearing capacity under three scenarios: the short-term scenario with adjusted severity, and the passive transition scenarios for 2030 and 2050 under SSP2-4.5.

Under the three aforementioned scenarios, most of the Company’s operating sites are located in low-risk areas. Based on the ratio of potential impairment to net asset value for owner-owned premises, the Company’s risk bearing capacity under each scenario is assessed at 2.73%, 1.30%, and 1.51%, respectively. The corresponding total potential impairment amounts are NT$1.491 billion, NT$709 million, and NT$823 million. Overall, the financial impact of physical risks on the Company’s owned fixed assets is assessed as low.

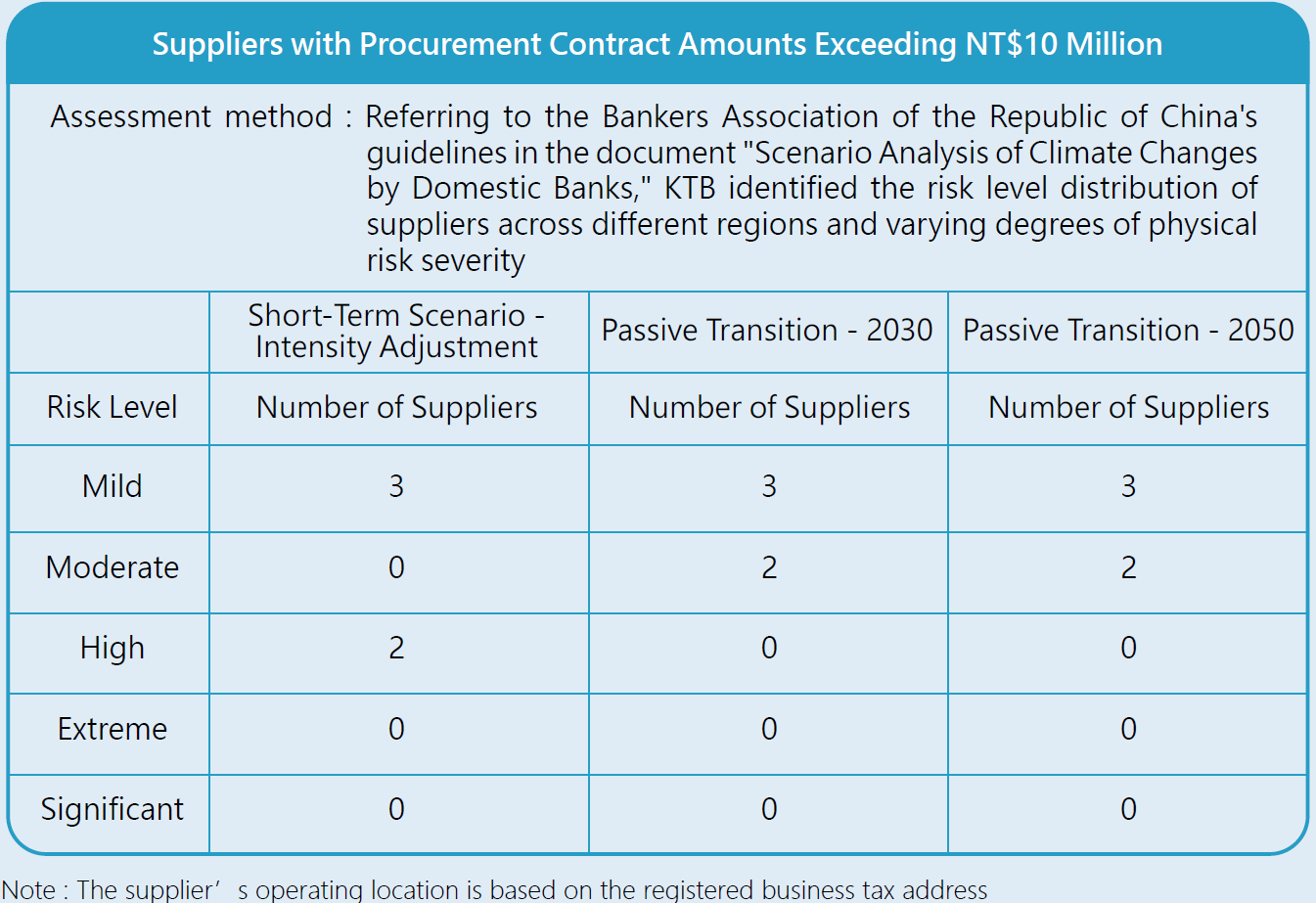

◆ Potential Supply Chain Disruption Risks

To understand the potential impact of extreme weather events on suppliers’ ability to deliver products and services as contracted, KTB evaluated suppliers with contracted procurement amounts exceeding NT$10 million in 2024. The assessment covered three scenarios—Short-term (Intensity-Adjusted), Passive Transition 2030, and 2050 under SSP2-4.5—focusing on risk level distribution to determine suppliers’ delivery feasibility during disasters. This serves as a reference for adjusting the Company’s supplier management strategies and further strengthening operational resilience.

Under all three scenarios, most of the Company’s key suppliers are located in low-risk areas.

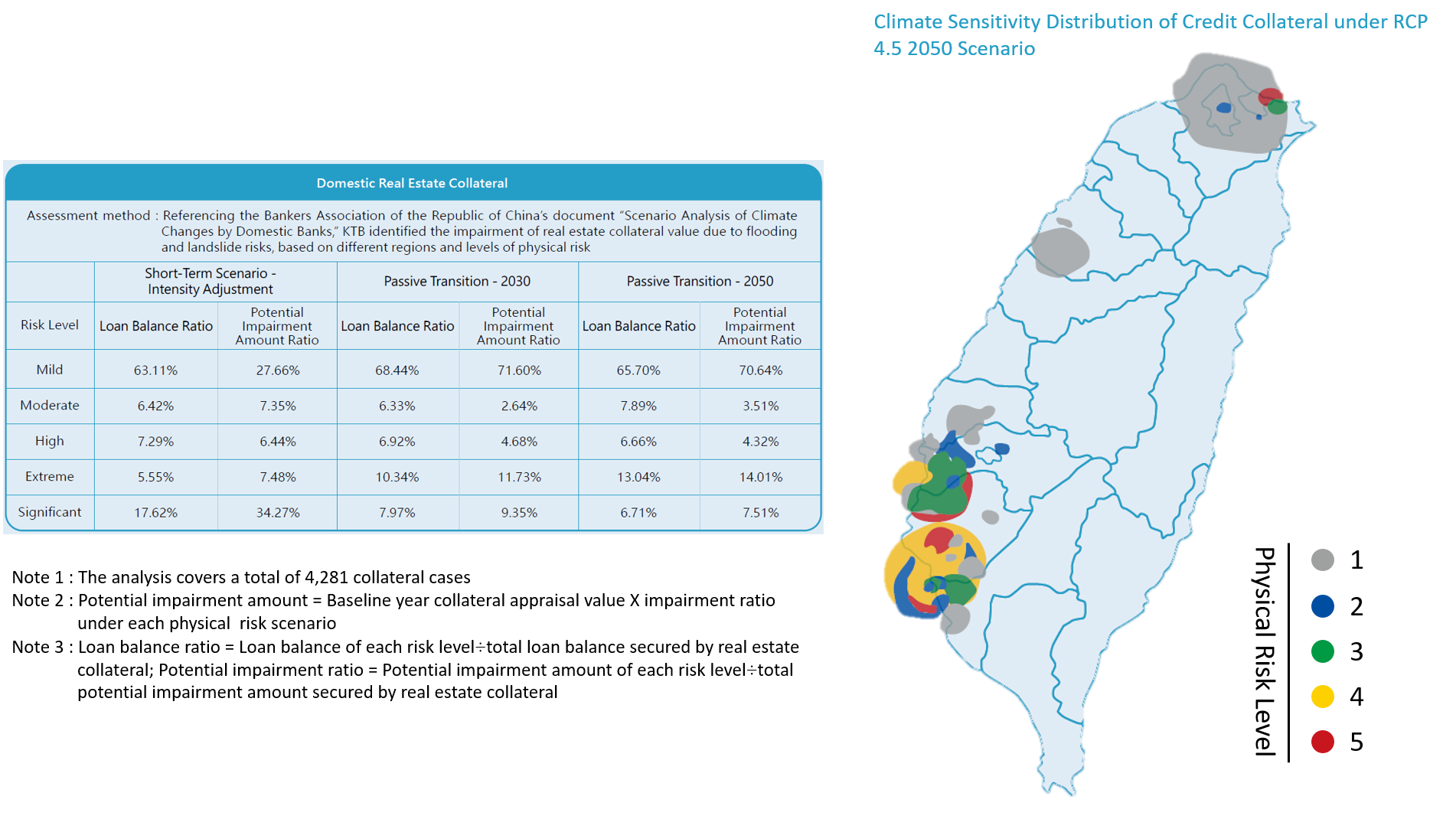

◆ Impairment of Domestic Real Estate Collateral

KTB primarily generates revenue from credit business, with real estate often used as collateral. Climate change has increased the frequency and intensity of extreme weather events, potentially reducing the value of real estate collateral associated with credit business. As a result, banks face an elevated credit risk. Consequently, KTB has recognized the depreciation of real estate collateral as a significant climate risk factor.

KTB conducted an analysis of real estate collateral located in Taiwan through its climate risk analysis database. The assessment examined the distribution of risk levels, potential impairment amounts, and loss-absorbing capacity of collateral under three climate scenarios: a short-term scenario - intensity adjustment, and the passive transition scenarios for 2030 and 2050 under SSP2-4.5.

Under the three aforementioned scenarios, most collateral falls within low-risk areas. Observing the potential impairment amount of collateral located in "significant" risk zones under the passive transition scenario, it accounts for approximately 7.5% to 9.4%, indicating that tail risks under the passive scenario remain within a controllable range. In the short-term scenario, the potential impairment amount of collateral located in significant risk areas accounts for 34.27%. This is mainly because, on average, the impairment rate of collateral in significant risk areas is 84.6% under the short-term scenario. When measured by changes in loan-to-value (LTV) ratios, the risk tolerance of loans secured by real estate under different scenarios shows an increase from the baseline year’s 14.95% to approximately 19.57%, 19.74%, and 18.73%, respectively. This indicates that the financial impact of physical risks on this business segment is relatively mild.

Transition Risk Analysis - Additional Costs from Carbon Pricing System

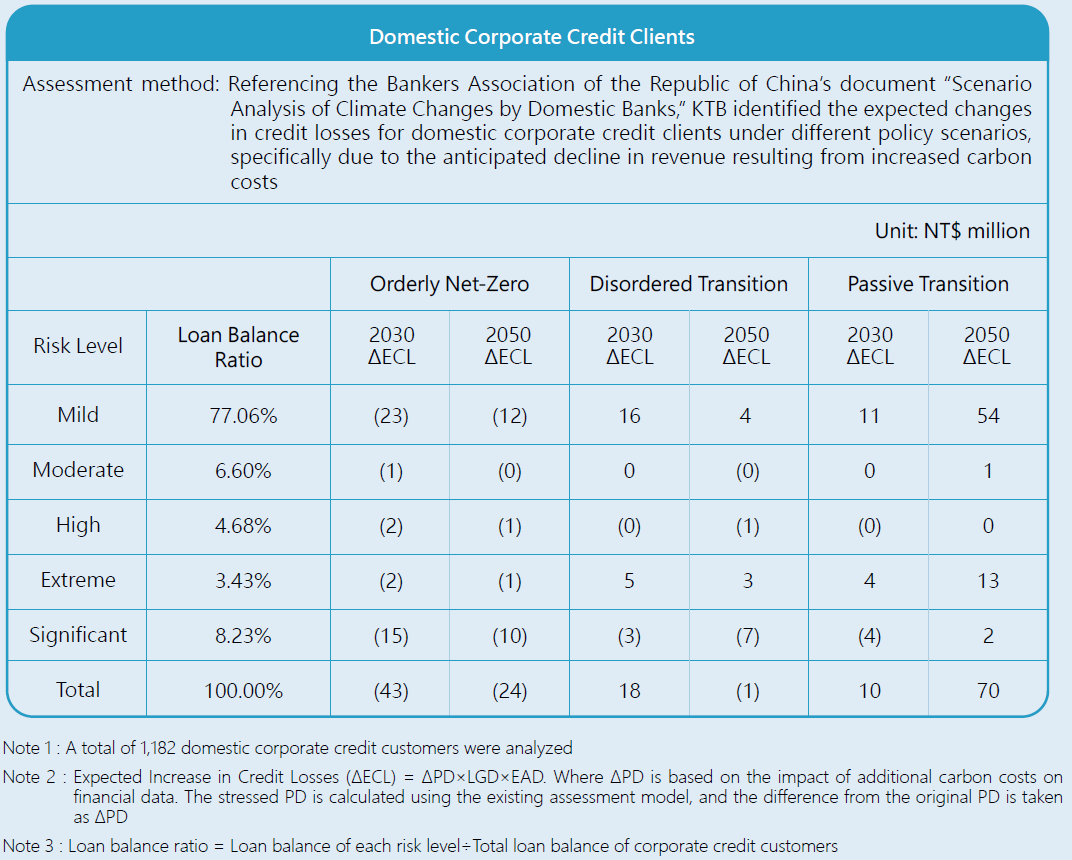

◆ Impact of Carbon Pricing on the Revenue of Domestic Credit Clients

In February 2023, Taiwan promulgated the "Climate Change Response Act." Subsequently, in August 2024, three supporting sub-laws were announced: the "Regulations Governing the Collection of Carbon Fees," the "Regulations Governing Self-determined Reduction Plans," and the "Designated GHG Emissions Reduction Goals for Entities Subject to Carbon Fees." Starting in 2025, Taiwan will impose a carbon fee of NT$300 per metric ton of CO2e on large emitters with annual emissions exceeding 25,000 tCO ₂ e, marking the official beginning of the carbon pricing era in Taiwan. In addition to the costs of carbon taxes/fees, enterprises must also comply with low-carbon transformation regulations. This requires making adjustments to production processes, supply chain management, or product design, which leads to increased expenses. As a result, the company's profitability is affected, and it may also impact the assessment of the company's repayment ability and the potential increase in credit risk by banks. Therefore, KTB has recognized the carbon pricing system as a significant climate risk factor.

KTB, in reference to the NGFS climate change scenario framework, analyzes the domestic credit business in the context of three scenarios: Net Zero 2050, Delayed Transition, and Fragmented World. The analysis examines the risk level distribution and expected credit loss changes for 2030 and 2050 under the scenarios of Orderly Net Zero, Disordered Transition, and Passive Transition.

KTB categorized the transition risk of its domestic credit business primarily as Level 1 - "Mild," accounting for approximately 77.06%. Based on the overall changes in expected credit losses, a further analysis of the Company's risk-bearing capacity under the Orderly Net-Zero, Disordered Transition, and Passive Transition scenarios for 2030 and 2050 is summarized in the table below. The results indicate that the financial impact of transition risks on this business segment remains within a manageable and controllable range.

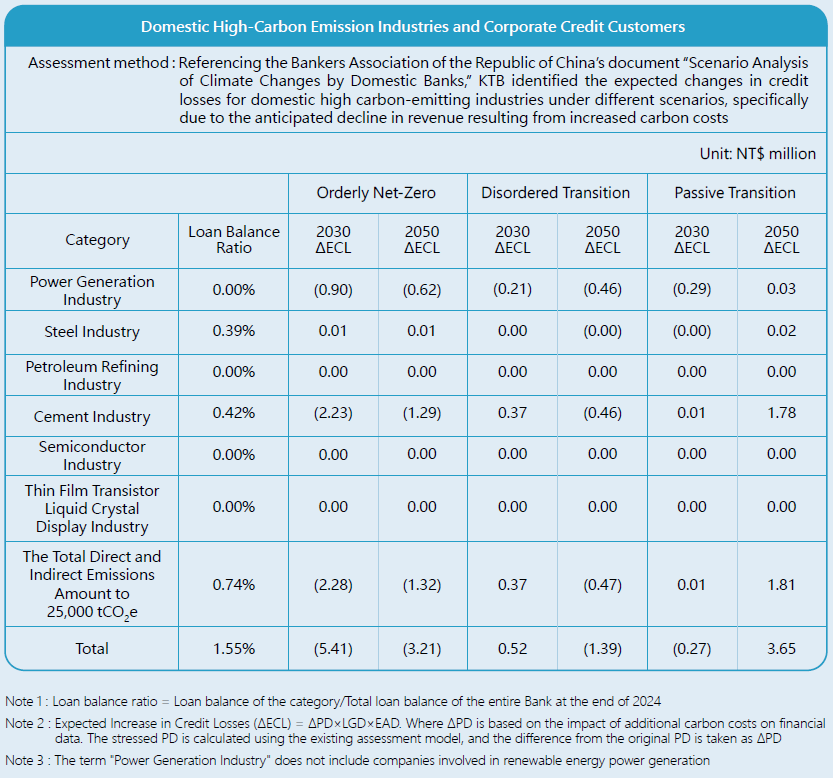

◆ Domestic High-Carbon Emission Industries and Corporate Credit Customers

Starting in 2025, Taiwan will officially enter the era of carbon pricing. In response to this policy, KTB has considered that the credit recipients are primarily domestic enterprises. Therefore, we have referred to the "Regulations for Gas Emission Inventory Registration and Inspection Management" and have classified the power generation industry, steel industry, petroleum refining industry, cement industry, semiconductor industry, and thin-film transistor liquid crystal display industry as "high carbon emission industries." In addition, we are tracking the total of 25,000 tCO2e in direct emissions and indirect emissions from electricity for credit customers. This is to enhance monitoring and control of transition risks under the carbon pricing system.

As of the end of 2024, KTB's domestic corporate credit customers classified under the aforementioned categories had a total credit balance of NT$3.965 billion, accounting for approximately 1.55% of the Company's total loan balance. With reference to the climate scenario methodology issued by the competent authority, and taking into account both carbon price changes and the impact of heatwaves on productivity, the expected credit loss variations under the Orderly Net Zero, Disordered Transition, and Passive Transition scenarios in 2030 and 2050 were analyzed. The results are as follows:

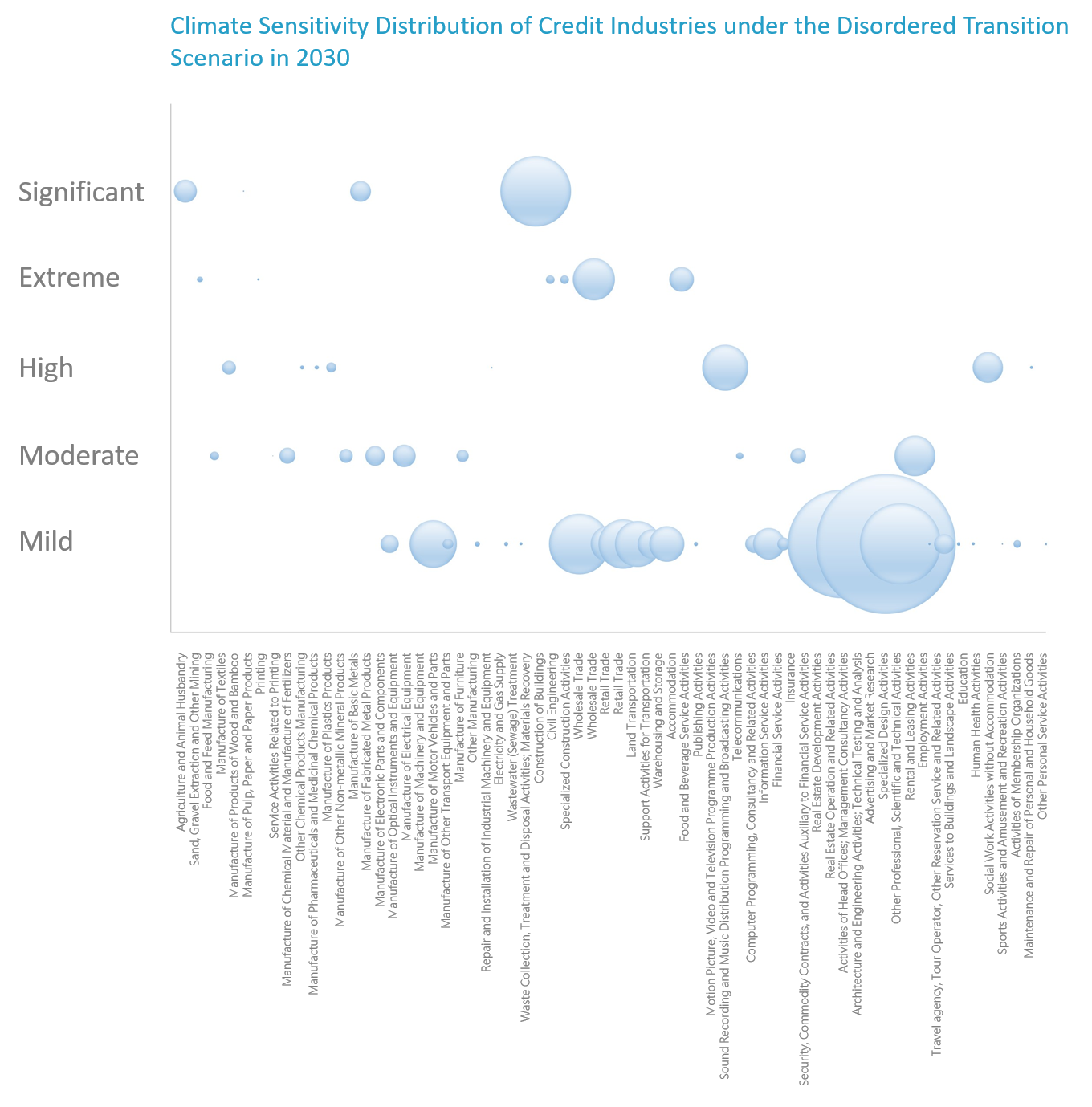

Scenario Analysis of High Credit Concentration Industries

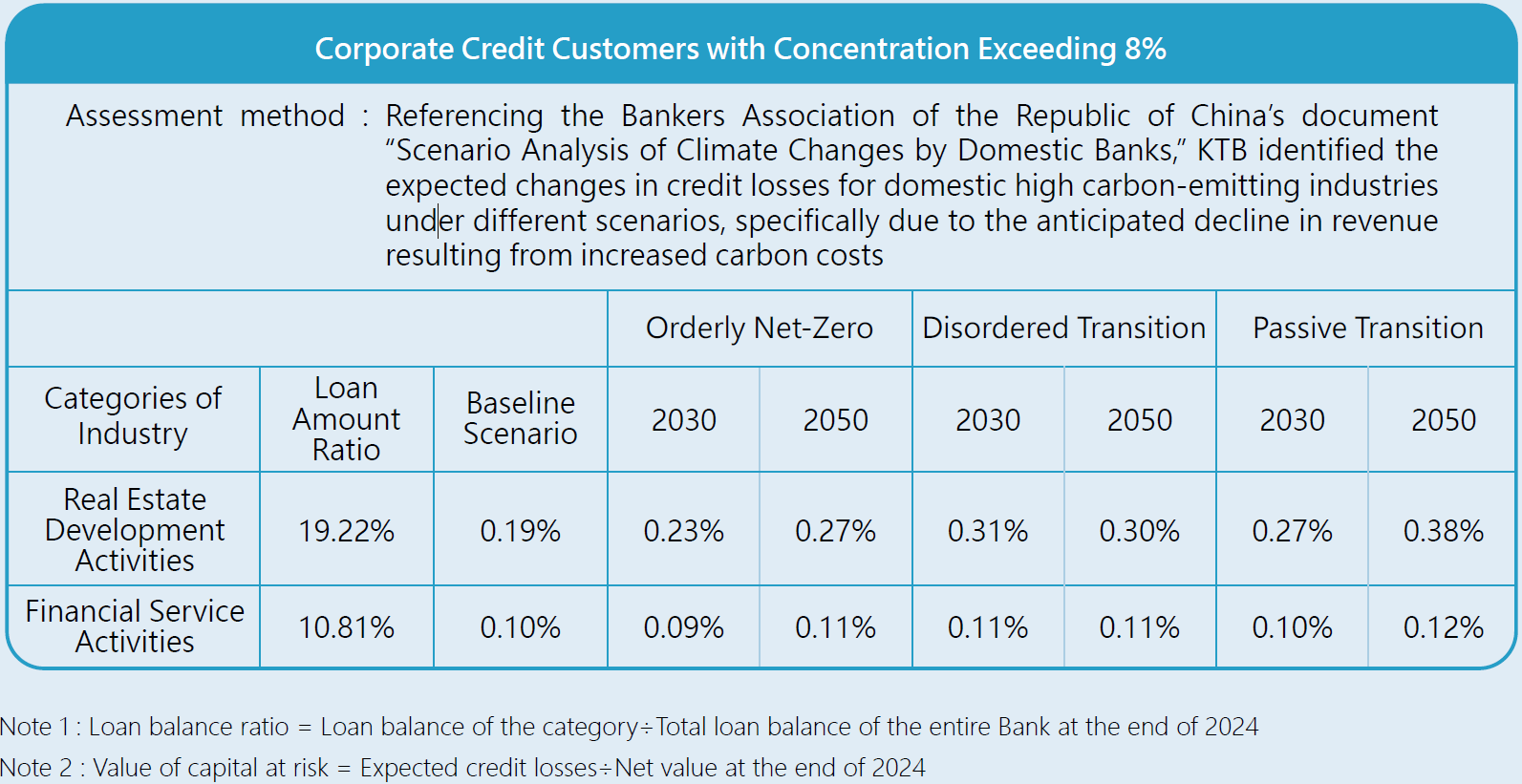

KTB primarily relies on credit business as its revenue source. To manage climate-related risks arising from industry concentration, industries with loan proportions exceeding 8% are further screened for analysis. The industries with concentration exceeding 8% at KTB are financial services and real estate development. The value of capital at risk performances in various scenarios for the years 2030 and 2050 are as follows:

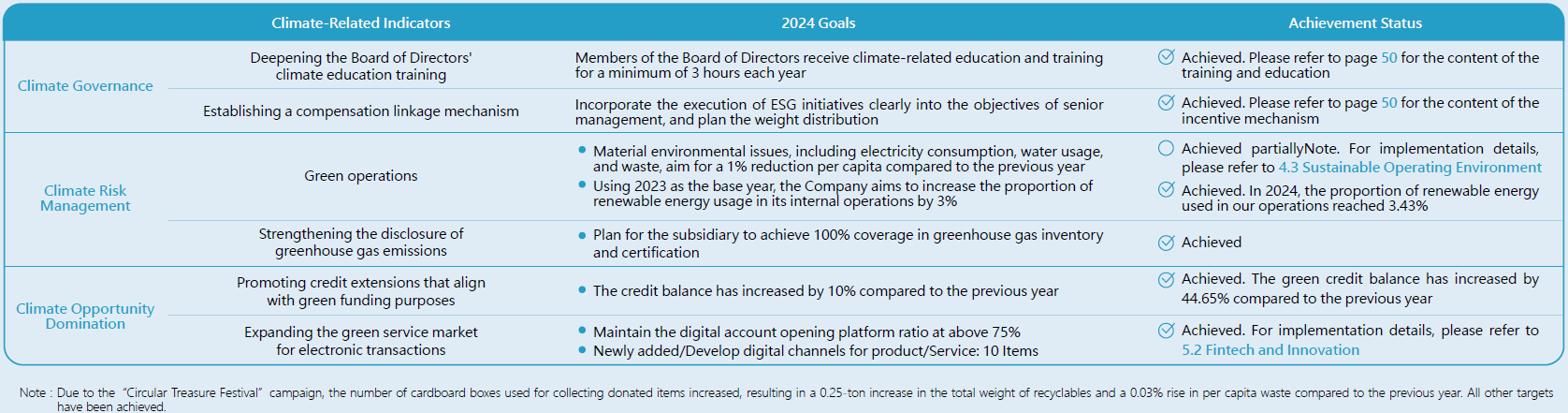

Climate-Related Indicators and Targets

KTB adopts a progressively deepening strategy in response to climate change and regards the establishment of climate-related indicators and targets as a foundation for strengthening management mechanisms and driving substantive action. In addition to implementing ISO 50001 Energy Management System, ISO 14001 Environmental Management System, and ISO 14064-1 Greenhouse Gas Inventory within internal operations to establish mechanisms for monitoring and improving key environmental metrics such as carbon emissions and energy efficiency, KTB has also extended its management focus beyond operational activities to encompass climate governance, climate risk management, and climate opportunity identification. These efforts aim to continuously enhance transparency in external communication and achieve the dual value of climate governance and business growth.